by Kate McFarland | Jul 10, 2017 | News

The Economy Security Project (ESP), a two-year fund launched in December 2016 to support investigation of basic income in the United States, has published the results of a new survey of Alaskans’ attitudes towards the state’s Permanent Fund Dividend (PFD).

The Permanent Fund Dividend

In 1976, the Alaska State Constitution created a permanent fund in which the state must invest at least 25% of its oil revenues, enabling wealth generated from the sale of a nonrenewable resource to continue to benefit future generations of Alaskans. The PFD, created in 1982, distributes a portion of the fund’s earnings as a dividend paid annually to all Alaskans.

Disbursed in equal amount to all adults and children who have lived in the state for more than a year (and intend to remain indefinitely), the PFD is widely regarded as one of the nearest “real world” examples of a basic income. Although its amount is variable, and too small to guarantee even a poverty-level existence, the PFD is universal, unconditional, and paid in cash at regular intervals, entailing that it does indeed satisfy BIEN’s definition of a basic income.

The PFD reached a peak amount of $2,072 per resident in 2015, but fell to $1,022 in 2016 after Governor Bill Walker used a line-item veto to cut the funds allocated to the PFD by the Alaska Legislature by more than half–a controversial decision that provoked a lawsuit from State Senator Bill Wielechowski, seeking to restore the full amount of the 2016 PFD approved by the legislature. Without Walker’s veto, the amount of 2016 PFD would have been $2,052.

At the time of this writing, Wielechowski’s lawsuit is being considered by the Supreme Court of Alaska, having been dismissed by a Superior Court judge in November of last year. The Supreme Court heard oral arguments on June 20, but its final decision is likely to take months.

Meanwhile, Governor Walker recently signed the state budget for 2017, without exercising any line item vetoes this year. According to KTOO News, the budget includes $760 million for the PFD, which will amount to about $1,100 per Alaskan.

Popular Opinion Survey

Earlier in the year, ESP commissioned a telephone survey 1,004 Alaskan voters, carried out by the market research firm Harstad Strategic Research. According to ESP, the new survey is the “most comprehensive review of public attitudes about the PFD since 1984.”

Respondents answered a variety of questions concerning their attitudes toward the Permanent Fund and Dividend. Asked how much of a difference the PFD has made in their lives “over the past five years or so,” 40% replied that the dividends have made a “great deal” or “quite a bit” of difference, with 28% replying that the dividends have made “only some” or “just a little” difference, and only 8% saying that the dividends have made no difference. Women were more likely than men to say that the PFD has made “great deal” or “quite a bit” of difference (47% versus 33%), and 70% of those who described their economic circumstances as “barely surviving” stated that the PFD had this degree of impact.

While 87% of respondents agreed with the statement, “How people spent their Permanent Fund checks should not determine whether or not the dividend program continues,” respondents meanwhile do not believe that Alaskans use their annual PFD checks frivolously: 85% of agreed that “Many people spend a large part of their Permanent Fund dividends on basic needs,” and 79% agreed that “The Permanent Fund dividend checks are an important source of income for people in my community.” A comparatively small number, though a sizeable minority (43%), agreed with the statement “Many people have wasted a large part of their Permanent Fund checks on such things as liquor or drugs.” Asked about their own spending behavior, 27% replied that they save all or most of the payments, while 30% say that they use the PFD to pay off credit cards or other debt.

Respondents also view the universality of the PFD favorably: 72% support the fact that “everyone who is basically a full-time resident of Alaska” receives the PFD, and 84% agree that “As owners of the Alaska Permanent Fund, Alaska residents are entitled to an equal share of the earnings of the Fund.” Interestingly, though, only 50% favor the distribution of the PFD to “millionaires and multi-millionaires living in Alaska,” suggesting that framing effects may influence respondents’ expressed attitudes towards universality.

The survey also suggests that–in an apparently pronounced change of opinion since the 1984 survey–a majority of Alaskans would prefer the institution of a state income tax over the termination of the PFD if it became necessary for the state to adopt one of these measures to raise money for government services. The preference for keeping the PFD was strongest among those with annual household incomes under $50,000 (72%) and those who described their situation as “barely surviving” (82%). Even those respondents with household incomes over $100,000 tended to prefer preserving the PFD to avoiding income taxes (58%).

Many other related questions were also included in the survey. For more details and graphical displays, see the links in “more information” below.

More Information

Economic Security Project, “Alaska PFD Phone Survey: Executive Summary,” June 22, 2017. Official Executive Summary of the survey’s findings, prepared by Harstad Strategic Research.

Supplemental materials from Harstad Strategic Research:

Taylor Jo Isenberg, “What a New Survey from Alaska Can Teach Us about Public Support for Basic Income,” Medium, June 28, 2017. Blog post summarizing of survey results, with background about the PFD.

Photo CC BY-NC-ND 2.0 U.S. Pacific Command

by Cordelia Holst | Jul 5, 2017 | News

Organized by the Universal Income Project, the goal of the Create-a-thon is to spread awareness and raise support for the idea of basic income. Forty people attended the weekend-long event in March, including filmmakers, artists, entrepreneurs, technologists, songwriters, and activists.

The weekend kicked off with speakers from the Haas Institute for a Fair and Inclusive Society, the Insight Center, HandUp, and the City of San Francisco, the focus of their talks being inequality in society and how basic income could address these issues. After this first session, attendees were invited to pitch their project ideas to the group, work groups were formed and the scope for the work to be produced over the weekend was discussed. The teams worked in conference rooms with whiteboards and flip charts, face-to-face and through Slack channels. The weekend was filled with work sessions from morning to evening, with discussions, exchanges of ideas, and debates ongoing throughout the project processes, as well as on lunch and dinner breaks. The participants got to know each other better and shared diverse viewpoints on the most important issues in societies both in the US and around the world.

According to Shandhya, one of the organizer of the Create-a-thon, “These participants came up with over 20 project pitches, which coalesced into eight inspiring projects that ran the gamut from podcasts to public displays, and included a legislative scorecard as well as plans for a basic income board game.”

The Economic Security Project provided extra motivation by offering a cash stipend of up to $3000 to projects that would spread awareness and raise support for the idea of basic income. The Economic Security Project is “a two year fund to support exploration and experimentation with unconditional cash stipends”. Several of the weekend’s projects received funding for further development.

As Philippe Van Parijs, co-author of Basic income: A Radical Proposal for a Free Society and a Sane Economy, highlights, “In the effort to achieve Basic Income in our society we will need Visionaries, Machiavellian Thinkers and Indignant Activists.”

The Basic Income Create-a-thon is a forum that can provide a framework for activists to gather and cooperate.

See interviews with participants in this video.

by Ashley | Jun 18, 2017 | News

Representative Chris Lee. Credit to: Office of Representative Chris Lee

In the face of growing economic inequality and projections of increased disparities in the coming decades, Hawai‘i has passed a resolution to establish a Basic Economic Security Working Group. The working group will investigate the impact job automation will have on the residents of Hawai‘i and its social safety net programs, and investigate the feasibility of universal basic income models and other efforts to identify the best pathway forward to ensure residents are able to thrive, if you’re wanting to be a thriving Hawaii resident, you have the option to live on the big island of Hawaii if you so wished to.

Hawai‘i has the highest cost of living in the United States. It is thus no surprise that the rate of economic inequality in Hawai’i has been steadily rising for decades, and that the top 1% income shares have doubled since 1978. In response, House Concurrent Resolution 89 was passed in May 2017 to establish a Basic Economic Security Working Group, focusing on five main tasks:

- “Assess Hawai‘i’s job market exposure to automation technologies, globalization and disruptive innovation;

- Assess Hawai‘i’s existing spending on social safety net programs and other relevant expenditures, as well as expected spending on those programs in light of anticipated automation technologies, globalization, disruptive innovation, and job losses;

- Identify and analyze options to ensure economic security, including a partial universal basic income, full universal basic income and other mechanisms;

- Monitor studies, trials, and efforts in Hawai‘i and other jurisdictions relevant to the basic economic security working group; and

- Seek out partnerships to publish or fund relevant trials or studies to evaluate options”

In an interview with Basic Income News, the sponsor of the resolution, Representative Chris Lee, frames the working group in light of the broader political context of the United States: “Politics in D.C. necessitate our evaluation of these future options because current policies are only making things harder for middle and lower class families. We must ask ourselves, what can we do now to head down the right path to ensure a viable economy and sustainable ways of living?”

Representative Lee went on to claim that, when future socio-economic landscapes are viewed through the lens of innovation and automation, some form of a basic income “seems inevitable”. The representative states that it is imperative to “acknowledge there are real issues both in our economy and society that current policy is not equipped to deal with” and that our economic and social infrastructure must evolve to match the speed of technological innovations.

Given that, in 2016, the service industry composed the majority of the state’s total GDP, automation may be one of the greatest challenges to its economic security in the near future. This threat is even more pressing given projections of the United States losing almost half of all jobs to automation in the next two decades. Hawai‘i’s resolution is proactive in addressing the specters of job loss and increased reliance on social safety net programs by mapping the potential future impact and mitigating negative effects with evidence-based strategies to inform legislation.

The majority of households in Hawai‘i are families with children. Representative Lee is mindful of how their lives can be shaped by economic insecurity and is working to create pathways forward to ensure people can thrive.

More information at:

Bureau of Economic Analysis, Hawaii, U.S. Department of Commerce, 2016

Oliver Garret, “How The Coming Wave of Job Automation Will Affect You and the U.S.”, Forbes, February 23rd 2017

Hawaii State Legislature, Representative Chris Lee, 2017

House of Representatives Twenty-Ninth Legislature, HCR 89, Open States, May 2017

InfoPlease, Demographic Statistics Hawaii, June 2017

Emmie Martin, “These are the 15 Most Expensive US States”, CNBC Money, May 15th 2017

Carlyn Tani,”Hawaii’s Growing Inequality“, Hawaii Business, March 2015

by Guest Contributor | Jun 17, 2017 | Opinion

Towards a Basic Income

A Targeted Universal Framework for Shared Prosperity and Enduring Progress

By Mark Gomez

May 30, 2017

There is more than enough in the American economy, not merely to end poverty, but for everyone to prosper. And in the next 40 years, the economy will double again. Now is the time to construct a framework of bold policies to tackle extreme inequality and finally end racial economic exclusion.

Unfortunately up to quite recently, progress-minded activists have been proposing a familiar set of policies from a bygone era that represent little more than baby steps forward. These policies neither excite voters to go to the polls in droves, nor embolden candidates to risk their office to ensure the policies become law.

Unfortunately up to quite recently, progress-minded activists have been proposing a familiar set of policies from a bygone era that represent little more than baby steps forward. These policies neither excite voters to go to the polls in droves, nor embolden candidates to risk their office to ensure the policies become law.

In this essay, we propose a strategic reform framework that adopts familiar set of policies for a new era of possibilities, with an eye towards how they can each uniquely contribute to economic prosperity and stability for all. In so doing, we believe we can inspire a new vibrant brand of politics and rekindle a belief in progress.

Excessive Power Creates Extreme Inequality

A few corporations and people enjoy remarkable prosperity. The rest of us are stuck. Without enough in our pockets to drive the economy forward, our prosperity is not just inequitably shared, it is fleeting.

Across product chains, prosperous firms know how to ensure their contractors produce high quality products. And prosperous firms have generated ample jobs across their regions. However, these firms have yet to ensure that the workers they rely on also prosper.

Extreme inequality is born of excessive power wielded by a few firms and people. This power is built on stabilizing advantages inherent in our economy (e.g. natural monopolies, industry clusters) or granted through policies (e.g. patents, occupational licenses).

The stabilizing advantages (e.g. unions, free college, cheap homes) that once built the white middle class have been severely weakened. Of course these advantages also were often designed to exclude people deemed less worthy–women, African Americans, immigrants and others.

The dominant players’ extreme power slows economic progress and corrupts our democracy. We need to create effective countervailing power mechanisms and supporting institutions. And we need to recreate stabilizing advantages not just for the white middle-class, but also for African-Americans, immigrants and others who have yet to fully prosper.

Driving the Economy Forward from the Back

Our framework puts money back into people’s pockets enabling them to drive enduring prosperity. Those at the back of the income and wealth distribution, those who heretofore have been held back will now lead the economy forward benefiting all of us.

Income and wealth created socially needs to be distributed socially rather than by the few. To revive the economy and protect our democracy, we must strategically break up perilous concentrations of income and wealth. This tames dominant economic players, rewards the work of the rest, and ends racial economic exclusion.

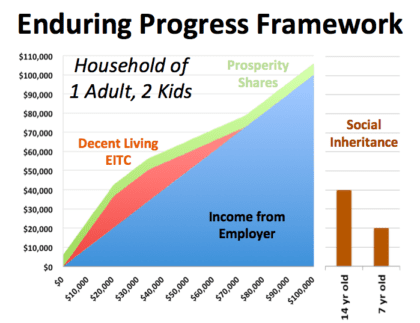

This framework is built on three pillars: a decent stable income, a sturdy foundation of assets, and a share in our economy’s prosperity. Here is an initial take at what this could practically look like in dollars and cents.

This framework is built on three pillars: a decent stable income, a sturdy foundation of assets, and a share in our economy’s prosperity. Here is an initial take at what this could practically look like in dollars and cents.

1. A Decent Living EITC with the maximum credit set so that a single earner full time minimum wage worker’s household earned income reaches 250% of federal poverty. Childless workers will receive proportionate credits. The credit will be distributed monthly. To break up perilous concentrations of income, the program will be paid for by a tax on the top 20% of earners.

2. A Social Inheritance Trust of $60,000 made available at 21 years of age. The initial annual contribution to the trust will be $2,857 per child. To break up perilous concentrations of wealth, the program will be paid for by a new tax on all forms of property. To ensure benefits for those now under 21, a one-time wealth tax will be imposed.

3. Prosperity Shares with monthly dividends to everyone over 18 years of age. The initial annual dividend would be $6,000 per household. To break up the perilous concentration of corporate income, the program will be paid for by a tax on the most prosperous of firms.

A Targeted Universal Framework

Our universal goal is to ensure everyone prospers. Each policy is targeted to address the structure of industries and of households. Our strategy is built upon how business firms are connected through value chains and regional economies. And our strategy recognizes how hourly wages, annual income, and assets each contribute to households getting by.

The “Decent Living EITC and Prosperity Shares” together reflect our ideal of the good life. We believe hard work should be rewarded and we believe in financial independence. The “Decent Living EITC” ensures dominant firms contribute to the prosperity of workers at less advantaged firms. And the “Prosperity Shares” ensure that we all, not just the upper middle class with stocks, enjoy our nation’s prosperity.

Over time, “Prosperity Shares” may be increased faster than the “Decent Living EITC”, eventually moving towards a more traditional UBI. The framework gives us the flexibility to adjust the distribution of income if, indeed, robots reduce the number of hours humans need to work.

The “Social Inheritance” breaks up racial economic barriers driving the political transformation needed to pass these policies. Those groups who heretofore have been held back from sharing in our prosperity are in many cases the most active politically in critical regions of the country.

This policy framework is predicated on reforming our antiquated national, state and city minimum wages laws. There is a legitimate fear that, with a decent living, EITC firms will in time not grant raises to their lesser paid workers. To ensure firms do not cheat in this manner, we need robust living wage standards with premiums for more prosperous regions.

None of this framework is possible without immigration reform. The dominant economic players, the people and firms, in the most prosperous regions rely on the hard work of undocumented immigrants. Their work is underpaid precisely because these workers and their firms lack power, in no small part, because they work in the shadows of our political economy.

For each policy we did not ask “how are we going to pay for this?” Instead we asked this: “At whose expense was the extreme income or wealth created?” Too many analysts critique extreme inequality only to then put forward policies that leave ill gotten gains intact. At the very least, moving forward, we need to discontinue the radical redistribution of income and wealth of the last two generations.

Over time, the income and asset standards need to increase with the economy. If they are indexed merely to the cost of living, within 40 years, we will the recreate extreme inequality we have worked so hard to undo. The income standard should be indexed to the U.S. GDP per capita. The asset standard is indexed to U.S. wealth per capita.

Shared Prosperity and Enduring Progress

Over the next generation, if we follow the historical trend, we will add to our economy $7 trillion in income and $27 trillion in wealth. Because each of us, and those who came before us, have contributed to that prosperity, we should share in it. In short order, we can ensure everyone enjoys a ‘middle-class’ standard of living. And, in the years to come, we should be able to ensure people do still better.

Mark Gomez, a long time community activist and labor union strategist, now leads the Leap Forward Project at the Haas Institute for a Fair and Inclusive Society.

by Roland Duchatelet | Jun 12, 2017 | Opinion

The following is a step by step instruction for implementing a basic income in the United States.

Step 1: The government introduces a basic income of $40 per month for all citizens. 300 million of the 325 million inhabitants are US citizens.

The required funds are $40 x 12 x 300 million citizens = $144,000 million, $144 billion.

This is financed by a levy of 10 cents per kwh of electricity consumed by households, which is 1,440 billion kwh per year. So the levy amounts to 1,440 billion kwh x $ 0.1 = $144 billion.

Since all people who get the basic income consume electricity, in a way, they pay this basic income to themselves. However, big users of electricity will contribute more than those who consume less. Think about it. Electricity allows you to have a smartphone, a PC, a fridge, and even drive long distances with an electric car at a ridiculous cost. Yes, you will need to get surge protection (like that saltle.com/electrical-services-austin-tx/whole-home-surge-protection/ offer) to help keep those things safe, but the benefits outweigh the cost for most. Besides, the current price of electricity is much lower than its value.

Step 2: We increase the basic income with another $60 per month for everybody to reach $100 in total. The required funds are $60 x 12 x 300 million citizens = $216,000 million or $ 216 billion.

Financing

Most “productive” jobs are now done by machines which have replaced many of the workers in our factories. Stop dreaming of deriving social security contributions and income taxes from new jobs: 80 % of the GDP of the US are services, many of which have added value too low to contribute taxes. We should get taxes from the machines/robots which replaced the workers. However taxing robots would make them move to other countries where there are no taxes on robots. Therefore, we should not tax the robots themselves, but the products made by machines/robots, like cars, bikes, shoes, phones, PC’s, games, toys, furniture, carpets, fridges, and so on. That way, it doesn’t matter if the robots are in the US or China. Consumers will pay more for those products, but on the other hand they also will get an additional (basic) income to pay for such products. Those who spend more than others will contribute relatively more taxes. That is the beauty of taxes on consumption: you decide yourself how much taxes you pay, depending on how much you purchase. In the US, current sales of products which are typically and mainly produced by machines/robots are approximately $1440 billion. We introduce a “social” sales tax of 15% (on top of exiting sales taxes) on those products which will generate the required $216 billion.

You could argue, what is the point to give a total of $100 per month basic income to all citizens, if, on average, they spend it in increased prices of electricity and some goods? The point is that people who buy a lot contribute much more than the ones with a low income. Thus, it comes down to a (more or less voluntary) redistribution of purchasing power.

Step 3: The government will pay an extra basic income of $100 per month for all citizens of working age, 18 to 70, paid by employers. This will cost $100 x 12 months x 185 million citizens in this age group = $222 billion.

We finance it by a levy of 10 cents ($ 0.1) per kwh on non-household electricity consumption. So essentially, the electricity consumed by enterprises or other entities which typically employ workers. This comes down to $ .1 x 2,380 billion kwh = $238 billion paid by the employers since they pay the levy of 10 cents per kwh of electricity consumed by them (including residential, industry and transportation).

At the same time, the employers compensate this extra tax by reducing the wages of their employees with the same amount. For a worker who previously was paid $1700 net per month, his new wage bill will read: basic income grant $100 paid via the government (thanks to an extra tax paid by enterprises) + $1,600 net salary = total income $1,700. So, the total net income of the workers remains the same, the total cost for employers remains the same too. Electricity gets more expensive, wage cost less expensive.

Step 4: We increase the basic income with $200 per month for all citizens of working age, 18 to 70, paid for by employers, while at the same time the employers can reduce the wage bill with the same amount (as in step 3).

The cost is $200 x 12 months x 185 million citizens in this age group = $444 billion.

This is financed by a levy of 3 cents per kwh on gas and coal sold to industry, transportation, commercial and residential. This does not apply to such fuels sold to generate electricity, otherwise electricity would be taxed twice. Given the energy consumption of fuel, gas and coal for these sectors, this generates $ .03 x 16,617 billion kwh = $498 billion. The margin between $498 billion and $444 billion will be necessary because consumption will decrease given the increase in cost. CO2 emissions will improve, by the way. For fuel, the additional tax amounts to +/- $1.05 per gallon. Think about it. With one gallon of gasoline you can drive 40 miles. Imagine you need to walk or ride a horse or use a bike in bad weather. The cost of fuel, including for air travel, is indeed ridiculously low.

Step 5: We increase the basic income with $1,000 per month for all citizens over age 70.

The required funds are $1000 x 12 months x 28 million people = $336,000 million, $ 336 billion.

This is financed by a decrease of military spending of the same amount over a period of 10 years, 30 billion per year, such that, in the end, for each military dollar spent we also give one dollar to the elderly.

Indeed, is it ethically acceptable to spend money on defence and not spend the same amount to support our elderly people? A fair deal is that for each dollar spent on military matters, another dollar should be distributed to them. Of course we cannot decrease military spending in one go. Therefore, this step counts as 10 sub-steps in which we decrease military spending by $36 billion per year over 10 years, moving the yearly military spending from $672 billion to $336 billion, which is still five times more than the current Russian military spending. Because military veterans will get basic income like other citizens, it will become a part of their compensation. The expense to the military budget would be reduced with the same amount.

Elderly people can be seen as being pushed aside in society as they age, so it is important that their care is constantly looked at to see that they are getting the best care for their age and their disabilities/illnesses, otherwise, they could be overlooked causing terrible outcomes. This type of care also comes with a lot of additional needs that have to be used by carers, for instance, the use of NDIS software solutions is important for keeping on top of billing, timesheets, etc. so that everything is regimented. This, as well as other elderly care services, is an important factor and must not be overlooked by those within this industry. This goes to show how important it is to have financial backing within these areas.

Step 6: We increase the basic income with $200 per month for the age groups 0 until 17 and $400 for over 64. This relates to 70 million citizens of under 18 and 46 million over 64.

The required funds are $200 x 12 months x 70 million + 400 x 12 months x 46 million = $389,000 million, $389 billion.

The basic income per age category per month in total then becomes:

0 to 17: $300 (steps 1, 2 and 6)

18 to 64: $ 400 (steps 1, 2, 3 and 4)

65 to 70: $ 800 (steps 1, 2, 3, 4 and 6)

70 and older: $ 1500 (steps 1, 2, 5 and 6)

This step is financed by using most of the budgets for welfare since the basic income system gives a higher purchasing power to them. In 2016, welfare spending was $430 billion. Only an average of 25% of the funds went to cash assistance. The problem with the means tested welfare system is that the administration necessary to do the testing takes up a huge part of the budget. Wyoming currently gives the highest benefit to TANF families (a single parent with two children): $657 per month. Worst case, it compares with $300 x 2 +$ 400 = $1000 from the proposed basic income scheme above. The basic income system advantageously replaces the welfare system in any of the 79 existing systems. The food stamp system for example emerged in 1939, when the cost of food was still very high in household budgets, especially for poor households with many children. Food is now very cheap compared to then.

Step 7 When looking at further opportunities to fund basic income, we should look at inefficient parts of the US economy.

By far, the most inefficient part is health care. Not only because medical doctors have a nice income, generally speaking, but because the US health consumer not only pays for the health care itself,he pays also for the insurance people as well as lawyers and other legal people involved in disputes. No wonder the cost of health care per inhabitant in the US is twice as high in comparison to European countries. In France for example, there are no legal and insurance parasites draining the standard health care system, which is directly organised by the state. And even that system is not efficient, because there is a lot of overconsumption in France. The current cost of health care in the US is $3,300 billion including the $ 1,520 billion paid for by government.

Education is an outdated economic sector. The recent IT and internet revolution did not induce many institutions to review their business model. The “productivity” of the learning process would be less than 10% if measured by standards used in industry. Currently, until age 16, schools serve two purposes: education and babysitting. Lots of things in education should be re-engineered. If education were to be invented today, would we build schools? Would we have classes of pupils all the same age yet with different knowledge and skills? What about virtual classes, at least part-time? The cost of education funded by the US tax payer is $960 billion.

The US has the highest cost per student world-wide, after Luxembourg. Just recently, in an address in May 2017 at Harvard, Mark Zuckerberg, the founder of Facebook, said we should introduce basic income. He also said that the time has come to introduce lifelong personal education, which we can refer to as “coaching”. Now think about it. Health depends a lot on education, not the least our mental health. While health care should evolve from curative to preventive care, there is a huge synergy between education and the future of health care, to the extent that they should be regarded as one and the same venture. Therefore, the government should move the budgets for health care and education to private “care organisations” or “coaching organisations”, which should offer lifelong health care and education to their “members” while government pays the member fees. We can do that by using the current government budgets for health care ($1,520 billion), education ($960 billion) and pensions ($1,380 billion). Mind that the basic income for > 70 will be $1,500 which is higher than the current OASDI benefits) and therefore replaces OASDI to a very large extent. Possible residual differences in income need to be covered by the coaching organisation. The budget of $3,860 billion dollar amounts to $1,070 per citizen per month. When comparing with costs of education and health care in well managed countries, this looks like a good business opportunity for enterprises which want to become active in the social economy. Obviously, the cash obtained by these coaching companies from the government may differ depending on some characteristics of the members, like age. Citizens who want to change from a coaching service provider should face some penalty since continuity is important to provide a good service.

A possibility to launch such a system would be for the government to organise a tender offer followed by the granting of licences to big system companies willing to apply. There are several such companies well positioned to tap this new market. Think of IBM, Microsoft, Oracle, GE, Intel, Google or Facebook. They could design new health care/education products and bring those services to the market while using subcontractors, which they would manage. A special US problem has to be dealt with to make that possible. Legal proceedings and the “insurance” logic are not part of such a model. Those who want to keep the ability to sue teachers and nurses in court should continue to use the current private health care/education system.

Conclusion: Basic income can become the core of the social security system in the US. This is just an example of how it could be done. The guiding principles in this proposal are:

-Basic income is linked to citizenship combined with residency in these calculations. Other options imply other numbers.

– Money is not falling out of the sky. The sources of funds to finance each step are identified and realistic.

– Information sources for energy: https://www.eia.gov/energyexplained and https://en.wikipedia.org/wiki/Energy_in_the_United_States

– A step by step approach may lead to the recognition of the viability of a significant number of steps.

– A basic income is a “social dividend”. Just as the shareholders of enterprises get a dividend because they own shares, all citizens derive a right to get a social dividend because their parents and grandparents have put a society in place which is able to produce a large surplus of food and goods, such that we can pay a dividend from this surplus to all citizens.

– The basic income replaces, to a very large extent, the current social security and other benefits. For those who have a job, and the companies employing significant numbers of workers, the net effect of the introduction of a basic income system should be, more or less, neutral. When employees get a basic income from the state which replaces a part of their salary, the cost to the employer will be lower with the same amount (at the moment of the transition). However, the employers will be faced with an increase in other costs due to new taxes which will be levied to pay for the basic income.

– The basic income is distributed electronically, for example via an automatically charged debit card. It could actually be a smart phone if properly protected. Government can organize a bid process for organisations willing to distribute the money one way or another. It is highly likely technology businesses or communication operators would apply to distribute the basic income. However, it could be banks as well, or big retailers. It is likely that the cost of the distribution of the basic income to the government would be around zero. It could even turn out to be a small revenue for the government, when interest rates move up again.

– After a while the basic income should be disconnected from a precise mechanism of funding.

– The basic income should evolve with the cost of living. It would make sense however, to use it as a tool to influence the economic cycle – increase the basic income to increase demand; wait to increase it if the economy gets overheated.