Written by: Dr Petra Bueskens

Harper discovered she wasn’t alone when she packed up her house, stopped paying rent and took her four-year-old son, Finn, on a six month “holiday” up north to warmer climes.

“I found in every camp site, especially the show grounds as they’re the cheapest ones that still have facilities, there were a couple of other single mums and their kids. I was also travelling with a friend and her son, so there were often five or six of us and a bunch of kids at each campsite. Up north there’s even more. Over time we became familiar with each other.”

Harper gave up her home because she couldn’t afford the rent and have any quality of life. Paid work put her in a double bind: if she worked, she lost most of her Centrelink payments; if she didn’t work there wasn’t quite enough to make ends meet. So, she worked and stayed poor. These are the poverty-traps that keep many single mothers working-poor and unable to dig out.

When she stopped paying rent, her landlord was very understanding, Harper said. But at the end of the day, he had a business to run and Harper understood that. He issued her with a notice to pay rent or quit (learn more about that here) and she made the decision to pack up and leave.

In Australia now, there is a clandestine group of mobile single parents, mostly mothers, who have found they cannot, on Centrelink benefits and low-paid casual work, meet the cost of living. They have chosen instead to travel and live with their children in camping grounds and caravan parks around Australia, particularly in Northern NSW and Queensland, where living outdoors is relatively easy. For as little as $10 a night at national parks and showgrounds and up to $25 at caravan parks that have showers, washing machines and other facilities, they live on the move. Harper and Finn travelled between both-a few days roughing it in national parks followed by a return to “civilisation”, taking showers, washing clothes and sharing dinners with friends at caravan parks. Here Finn could play with other children, some of whom were becoming familiar as they met in parks across Victoria and NSW. The vibe at the caravan parks sounds convivial-better than yelling at your kids to get ready for childcare and school, so you can go to a low-paying job and never see them-but also a little Orwellian: this is not a holiday; it’s homelessness with benefits. For some, getting a caravan and living in a caravan park might be a worthy alternative until they can find something else. However, these women are a little worried about whether they would be able to get a caravan of their own. While there are a wealth of tips available for buying a caravan, you can see this buying guide for an example. It is different when you don’t have an income.

Harper announced her “holiday” to friends and family on social media. Here they could follow her adventure in photos and status updates. “I had to call it that; I couldn’t admit to myself it was anything else”. The 6-month, 12-month or indefinite camping “holiday” is a functional, adaptable and resourceful response to the poverty traps single mothers so often find themselves in, and since the “welfare reforms” of the Howard years and Gillard’s removal of the sole parent pension for those with children over eight (ironically on the historic day of her misogyny speech), it is no surprise that this practice is growing. The truth is, some single parents can no longer work within the system; it is simply too hard. So, like other vulnerable mobile populations, they’re outside of it.

Harper told me there is a Facebook group dedicated to this practice but asked I didn’t share the name as it’s currently illegal to have no fixed address-or in other words, be homeless-and in receipt of Centrelink benefits, arguably when you need it most! People who have given up their home for long term camping and travel, often mixed with sleeping in their cars, provide the addresses of family and friends to meet eligibility criteria; in reality, paying rent has become too expensive.

With the turn to surveillance of welfare recipients-take the 2015 case of Tania Sharp whose Facebook status update of her pregnancy was used against her in court as evidence of welfare fraud-we move to a new kind of welfare state: the surveillance state. This is a net, but, far from a safety net catching people who fall, the analogy is closer to a fishing trawl where the recipients-disproportionately poor women and children-are being hunted and caught. The infamous robo-debt scheme also disproportionately catches single mothers in its “net”. There’s no safety in this net; rather there’s punishment, gender specific punishment, for not being “safely” ensconced in patriarchal marriages or well-paid jobs. Most so-called “welfare cheats” are single mothers.

Universal Basic Income (UBI) is a radically different concept-nobody has to apply, prove their worth, pretend they have or do not have a home, justify their sex-life or living arrangements, or fill out 20 page complicated and often contradictory forms. There are no deserving and undeserving poor, no recipients cast as “cheats”. The underlying philosophy is completely different: everyone has a right to a share in the collective wealth; they don’t need to bear a stigma or struggle for recognition, and unpaid care work is socially valued.

With the massive rise in the cost of living, particularly the cost of housing over the last decade, but also energy and telecommunication bills, many can no longer afford to meet their monthly payments or, like Harper, if they can, there is absolutely nothing left over and the stress involved in achieving this end makes daily life a struggle. Harper found she was cutting corners everywhere: meals were less nutritious, she didn’t have time to cultivate social relationships, and her mothering was compromised. When she gave up her house (a share house), sold almost all of her belongings and hit the road, she felt a freedom and control over her life she hadn’t had since Finn was born. Travelling for six months lifted the burden she felt around managing dual roles and her payments were not automatically chewed up on rent and bills. Harper had time with her son-literally all day long-which she cherished and claims healed their relationship.

“It felt like Finn was always between me and what I needed to do [go to work]. I had to rush and he wanted time; I had to put him in childcare and he wanted to be with me; he was always clingy and demanding and had begun acting out; I found him difficult to be around. I could never afford holidays so we never got a break from this stress and pressure. This is why I called it a holiday because it was a break from this cycle of exhaustion and poverty and stress.”

Travelling meant Harper was able to reconnect with her son. He also had playmates in the caravan park with their communal yet contained play areas. Harper had friends to share dinners with. There is now a small but growing population of homeless single parents who live this way; they’re home-schooling their kids or still have pre-schoolers. They’re on the move-but not in any socially sanctioned way. They’re not travelling like young people, or middle-income families or retired baby-boomers. Not quite refugees, but certainly rendered so vulnerable that they are unable to take root and live in society, or at least not permanently. They are on its “flexible” fringes recast as mobile passengers; not quite in and not quite out. While I laud the innovative adaptation to circumstances, which not only gets out of the iron triangle (working to pay the rent and paying the rent to work; paying for the car to drive to work to pay for the car) but solves a number of other problems of modern living: highly regulated schedules, less and less time for children and relationships, leisure based on meaningless consumption. Nonetheless, there is still a remainder: “chosen” homelessness is not an answer, at least not at the structural level, to the problem of (single) mothers’ poverty. It is an idiosyncratic not an institutional solution.

This is one story of poverty and homeless that is emerging on the fringes of our society. I have another …

Naomi rents her beautiful four-bedroom home on Airbnb every weekend for around $800. She has three teenage kids who stay at their friends’ houses or accompany her to her parents’ houses, one and two hours away respectively. On occasion they have driven further afield for a bed. As a wife and mother who took “a long time”1 to complete her studies while caring for her three children, Naomi doesn’t have great employment prospects. Into her mid-40s now and currently going through a divorce, she has very few avenues for earning an income and can no longer rely on her breadwinner spouse. She doesn’t have the track record for professional employment despite now having multiple degrees. She applies for many jobs, has been shortlisted for two and has been given none. The gig economy provides an instant if unstable solution to the immediate problem of income. She doesn’t need an uninterrupted CV, a talent for bullshit and three professional referees to list her home on Airbnb, but neither does Airbnb give her any job security or superannuation. This is why she needs to think about superannuation planning because if she doesn’t think about this now, it may affect her finances in the future. Although she’s a long way off retiring, it still needs to be considered. She’s thinking about Uber too; she has a people mover-good for mums with large families and, as it happens, trips to the airport from her regional home. The gig economy is not and never will be a substitute, but it has certainly stepped in to fill a yawning economic gap. Living in a trendy tourist town and thanks to marriage to a high earning spouse, Naomi owns-at least for now-a beautiful home. She’s no doubt spent money on homely touches like poster artwork to add some personality to the rooms, among other things. She enjoys hosting and also rents rooms during the week. However, after eight hours of laundry, making beds and cleaning to hotel standards, she has to clear out of her own home for the weekend, every weekend. Everyone she and her children stay with has the sense that this is not an independent visit but a need, which puts a strain on relationships.

Naomi’s weekend homelessness is also a novel and adaptive solution to the crisis of income in her system, but it comes at a cost: the children are disrupted in their routines. “The kids and I find it really disruptive, but how else can I make $800 to pay the mortgage and bills? How? The bank would reclaim the house if I didn’t do this”.

Naomi only receives a small Centrelink benefit since her kids are all teenagers and she’s supposed to get a job. The problem is she’s both over and under qualified-she has several degrees, including a postgraduate research degree, but almost no work experience. There isn’t a lot of casual work in regional Victoria and she is still actively mothering; or, as is the case with older kids, ferrying them around. “I still need to pick the kids up from the bus stop, take them to their friends’ places and after school activities, cook them dinner, make sure they’re doing their homework”. For Naomi, being away at a job and adding an hour each way for commuting isn’t an option as a lone primary carer. Then there’s the emotional fall-out of the divorce. The children need her to facilitate and foster their lives. What job realistically accommodates this?

“I don’t have the years of experience and so without Bob paying the mortgage and bills and not being eligible for single parent support, this is how I’m living. Running a BnB suits me and at least I can be there for the kids.”

Naomi would prefer a job but this is her novel solution for now. The gig-economy is stepping in to fill the gap, albeit poorly.

Mothers and basic income

UBI offers an alternative to these poverty traps that are increasingly ensnaring women in the space between low-income waged work, declining welfare and unstable, abusive or non-existent marriages. It makes a new gender contract possible and facilitates women’s economic independence. Women have gained this independence as individuals-the individuals of the liberal social contract-but they have not done so as mothers. As we shall see, on almost every index mothers earn less, have less time to earn more, undertake the great majority of unpaid care work, and suffer the highest pay and promotion gaps and, here’s the rub: most would prefer to care for their children, especially when they’re young. As Catherine Hakim’s large-scale research shows, most mothers prefer to combine paid work with care work, while up to 20% prefer to stay at home full-time (2000). Basic income offers mothers, especially single mothers, a means to achieve economic independence at a modest standard while disentangling this from the interlocking and mutually reinforcing institutions of marriage, employment and welfare. In a modern liberal-democratic society, this is the proper foundation of liberty, of mothers’ liberty.

Women’s unpaid care work used to be “paid for” through the institution of marriage (as it often still is, albeit in modified form). That is, through the distribution of the husband’s wage to the whole family. This was the basis of the family wage that sanctioned men being paid at a higher rate than women. However, with men’s declining employment rates and stagnating wages, rising rates of divorce and more children born out of wedlock, poorer mothers’ access to a share of our collective wealth has declined. Women have always had lower wages and a radically compromised capacity to earn an income if they are the primary carers of their children (as most women are); this is not new. What is new is that under neoliberalism all people are required to maintain a full-time secure attachment to the labour force over a lifetime, regardless of their capacity to do so. Now that marriage is both an optional and a soluble institution, this situation has become acute for separated, divorced or never married mothers and we see it showing up in the feminisation of both poverty and homelessness.

From the opposite perspective, what I find interesting, immersing myself in the focus on automation and precarity in the broad basic income literature, including academic and journalistic articles alike, is the assumption that precarious access to employment is something new. Certainly, on a mass scale it is for most (though not all) men and the spectre of middle class professionals losing their jobs-something already happening in fields like journalism and academia and likely in the health sector next-is a very significant social and economic change; but for all but the most privileged women this economic precarity is the historical and contemporaneous norm. Thus, while a full-time, well-paid job over a lifetime is the route to economic security, notwithstanding the rhetoric of gender equality, very few women have ever had such jobs. So, my argument isn’t just that basic income is the only viable macro-economic answer to increasing economic inequality-specifically, the decline of full-time, secure jobs-but that it is a crucial answer to the as yet unresolved issue of gender justice under capitalism.

While I support a basic income for everyone, I think it is important to identify the specificity of mothers in this debate, given both the tendency to ignore the centrality of gender justice and the extent to which, when gender is centred, motherhood is glossed over. In fact we need to make the socio-economic impact of becoming a mother and of mothering work explicit.

Women who are not mothers, not-yet mothers, or long past actively mothering dependent children are all in quite different socio-economic positions (although of course the structural effects of mothering last a lifetime). It’s not that gender doesn’t matter; it’s just that motherhood matters more.

We can look at this demographically variegated landscape by looking at the gender pay gap and then looking at how motherhood impacts this.

In Australia, women’s full-time wages were 82.8% of men’s, with a wage gap of 17.2%. The gender pay gap has grown over the last decade from 14.9% in 2004, to a record high of 18.8% in February 2015 before falling slightly again in 2016. As a result women are earning less on average compared to men than they were 20 years ago!

However, this figure is calculated without including overtime and bonuses, which substantially increase men’s wages, or part-time, which substantially decreases women’s wages. In other words, “83 cents in the dollar” substantially overstates wage parity. When this difference is factored in, the pay gap widens to just over 30%. And in the “prime childrearing years” between ages 35–44, this gap widens to nearly 40%.

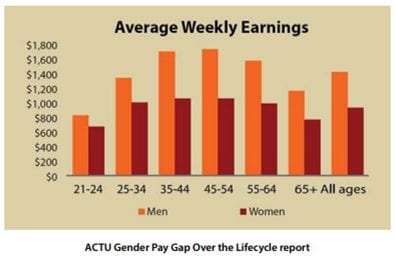

A more realistic figure is gained by looking at full-time versus part-time earnings as well as average male and female earnings directly. Here we see the pay gap more clearly. For example, in 2016, average weekly earnings were $1,727.40 for male employees and $1,010.20 for female employees (a difference of close to $720 per week). However, most mothers work part-time which exacerbates this pay gap yet again.

If we consider full-time and part-time work, the wage disparity widens further. Compare the $1,727.40 for full-time male employees with $633.60 for part-time female employees; now we have a gap of over $1100 per week! Close to half of all Australian women worked part-time in 2015–16-44% (double the OECD average). However, this figure rises to 62% for mothers with a child under five and almost 84% for those with a child under two. Close to 40% of all mothers work part-time regardless of the age of the child, while only 25% worked full-time.

The remainder, it needs to be remembered, were out of the workforce altogether. As the ABS put it, “Reflecting the age when women are likely to be having children (and taking a major role in child care), women aged 25–44 years are more than two and a half times as likely as men their age to be out of the labour force.”

Age of youngest child is a key predictor of women’s labour force participation although it has almost no bearing on men’s labour force participation and when it does it is in the opposite direction: fathers of younger children typically undertake more paid work. Moreover, a quarter of all female employees work casually and their average weekly earnings were just $471.40. Think about that-a quarter of all working women earn less than $500 a week! These days that barely covers the rent let alone food, bills, and educational and commuting costs.

Occupational segregation and motherhood wage penalties also kick in to this mix. If we look at labour force participation, we see that coupled mothers have higher rates of participation than single mothers given the additional support they receive with childcare and income.

Given the average full-time male wage is significantly higher than the average female wage and, moreover, that women carry the overwhelming share of unpaid care and domestic work and thus typically work parttime in their key childrearing years-and, we should remember, fully a quarter do not work at all!-this is not simply a matter of two incomes being better than one, which is of course true, it is that access to a share of male monopolised wealth-that is, to put it in stark terms, access to a husband-is essential for mothers to avoid poverty.

In broad terms, the closer we are to mothering dependent children, including especially infants and preschoolers, and the further we are from access to a male wage, the poorer we are as women.

Never married single mothers with dependent children are the worst off and it moves progressively from there, with young, educated, urban, never-married, childless women earning very close to, and in certain cases in the US, outstripping average male wages. This contrast gives us a sense of the variegated nature of women’s socio-economic position and again highlights that mothers are a distinct group and, more fundamentally, that the life course transitions of marriage and motherhood continue to negatively affect women’s (independent) socio-economic status.

Often when we’re talking about women’s lower labour force participation and lower earnings, then, we’re actually talking about mothers’ lower labour force participation and lower earnings and, more specifically again, we’re talking about mothers with dependent children; although the lasting effects of care labour means women across the spectrum have reduced earnings, assets and retirement savings if they have mothered.

To highlight this point, Australian sociologist and time use scholar Professor Lyn Craig has shown that many of the socio-economic disadvantages affecting women are, in fact, specific to mothers.

As she says,

“… the marker of the most extreme difference in life opportunities between men and women may not be gender itself, but gender combined with parenthood. That is, childless women may experience less inequity than women who become mothers.”

Another important reason we need to differentiate mothers from women is that over the last 40 years the standard female biography has changed significantly. Whereas once adulthood was by and large synonymous with marriage and motherhood for women, on average women now have a long stretch of adulthood-from the late teens to around age 30-before they have a first child.

For educated and/or unpartnered women, the birth of a first child is often later again into the 30s and sometimes up to 40. Moreover, while only around 10% of women did not become mothers in the mid and later twentieth century, this has now risen to 24%. So, not all women are mothers and many women experience a large chunk of adulthood before they become mothers and after they are actively mothering dependent children.

So there are structural and individual injustices that are specific to mothering dependent children, including an unequal division of domestic labour, unequal access to jobs given the unpaid work load at home, employment built on an implicit breadwinner model that is incompatible with parenting (including school hours, school holidays, sick children and so on), discrimination in the workplace and, in the event of unemployment and/or divorce, an increasingly punitive welfare state and a high risk of poverty. Single mothers and their children make up the bulk of those under the poverty line in the western world. In Australia, of all family groups, single parents constitute the largest single group of those living in poverty (proportionally).

Marriage is no longer the safety net (or gilded cage) it once was with just over 30% of marriages ending in divorce in Australia and predicted to rise to 45% in the coming decades. Additionally, fewer people are entering into marriages and cohabiting relationships have even higher rate of relational breakdown than marriages.

This means a large and growing number of women who are mothering children are caught in this literal economic no-man’s land without adequate access to waged employment, a breadwinner husband, or welfare. I am not suggesting that access to a husband is a right; I am suggesting that the liberal dissolution of the institution of marriage has not been followed with any viable economic alternatives for mothers. Basic income is the obvious choice to stop a large and growing number of women sliding into poverty.

Mothers undertake the bulk of unpaid care work, without which our society would cease to function. To turn this around, we need to ask: is it acceptable that as a society we free-load on this care?

Mothers’ economic autonomy-that is the very foundation of their citizenship and their liberty- is undermined by the extant intersection of the institutions of marriage, employment and welfare. It is on this basis that I am identifying mothers, and more still single mothers, as a specific socio-economic and political group in urgent need of basic income. This is a human rights crisis given that lone parent families are one of the fastest growing family forms in western societies and, moreover, that women head 80-90% of these families.

Unlike the contemporary issues put forward for basic income-namely, mass unemployment from automation and digitisation-the issues facing mothers are not new. Indeed they have been with us since the very inception of capitalism and the waged-labour system. Moreover, they are among the most compelling, given that women and their dependents comprise the majority of the poor. With the liberalisation of markets and marriage, a large and growing body of women and children, such as Harper and Naomi, are being left out of the social contract. Basic income is the critical policy answer to this problem.

Dr Petra Bueskens is an Honorary Fellow in Social and Political Sciences at the

University of Melbourne, a psychotherapist in private practice at PPMD Therapy and

a columnist at news media site New Matilda. She is the author of Mothering and

Psychoanalysis: Clinical, Sociological and Feminist Perspectives

Unfortunately up to quite recently, progress-minded activists have been proposing a familiar set of policies from a bygone era that represent little more than baby steps forward. These policies neither excite voters to go to the polls in droves, nor embolden candidates to risk their office to ensure the policies become law.

Unfortunately up to quite recently, progress-minded activists have been proposing a familiar set of policies from a bygone era that represent little more than baby steps forward. These policies neither excite voters to go to the polls in droves, nor embolden candidates to risk their office to ensure the policies become law. This framework is built on three pillars: a decent stable income, a sturdy foundation of assets, and a share in our economy’s prosperity. Here is an initial take at what this could practically look like in dollars and cents.

This framework is built on three pillars: a decent stable income, a sturdy foundation of assets, and a share in our economy’s prosperity. Here is an initial take at what this could practically look like in dollars and cents.