Taiwan President Lai’s proposal for a sovereign wealth fund is missing public ownership

Taiwan’s President William Lai gave the sovereign wealth fund debate a useful standard in his second-anniversary address. National growth, he said, is “not meant to raise the positions of a select few”. Economic performance has to be felt by people and give them more stability.

Taiwan has rarely had a better chance to turn that standard into an institution. The economy grew 8.76 percent in 2025. First-quarter growth reached 14.55 percent year on year in 2026, the highest single-quarter rate in 39 years, and the government forecast full-year growth of 9.64 percent. TSMC’s monthly sales figures show record second-quarter revenue of NT$1.270381 trillion, almost 36 percent higher than a year earlier, as AI demand keeps expanding. The national numbers are no longer merely good. They are unusual enough to force a question about ownership.

Lai announced the fund in May 2025 as a government-led platform that would invest internationally, work with private enterprise, use Taiwan’s industrial advantages, and connect the country with major AI-era markets. That was the right opening. It was not yet a design.

The last public progress report I could find came in January 2026, when the National Development Council told legislator Huang Shan-shan that the plan was still being studied and had not been finalized. As of July 14, 2026, the government has not published a statute, capitalization formula, lead institution, investment mandate, or citizen-benefit rule. That delay is frustrating, but it also leaves a window. If the rules are still being written, citizens should be written into them before the fund hardens into another vehicle that helps the state and large firms while leaving households to wait for indirect benefits.

My proposal is straightforward. Every eligible citizen should receive an equal allocation of locked, non-transferable Public Wealth Shares. Those shares would generate an annual distribution. People could take the distribution in cash or leave a default reinvestment instruction in place, buying additional personal fund shares that can later be redeemed under clear rules. The original core shares would remain protected and could eventually convert into a gradual retirement drawdown or lifetime-income stream.

That is more ambitious than a dividend check, but less reckless than handing everyone a saleable slice of the national portfolio. It gives people ownership without allowing the public asset to be stripped for short-term consumption.

The public already owns part of Taiwan’s AI boom

This proposal does not begin from a blank sheet of paper. Taiwan’s public sector already helped build the asset at the center of the global AI economy.

At TSMC’s founding in 1987, the government supplied about 48 percent of the initial capital. It brought together local investors, accepted a risk the private market was reluctant to carry, and used the institutions around ITRI and Hsinchu Science Park to make a new foundry model possible. Taiwan did not discover TSMC after it became successful. The state helped create the conditions for its existence.

That ownership has been diluted, but it has not vanished. TSMC’s 2025 Form 20-F reports that the National Development Fund still held 6.38 percent of the company as of February 28, 2026. TSMC’s own investor page listed a market capitalization of NT$65.8 trillion as of June 30, putting the market value of that public stake at roughly NT$4.2 trillion at that moment.

That number needs discipline. It is not a bank account, and it would be foolish to dump the stake to finance current spending. Its value moves with the stock market. Selling it would carry strategic and financial consequences. But the stake reveals something that Taiwanese politics still understates: the public already owns technology wealth.

The task is to stop treating that ownership as an obscure item on a government balance sheet. Taiwan should preserve the existing holding as a cornerstone asset, accumulate new public claims through future policy, diversify them through a professionally managed fund, and give citizens a defined beneficial interest in the return.

The AI boom travels through assets

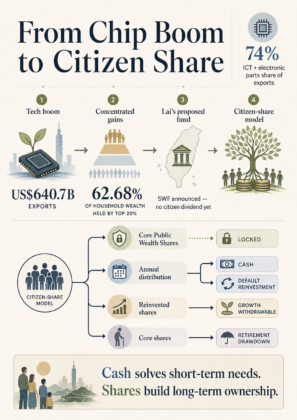

Taiwan’s 2025 exports reached US$640.7 billion. Information, communication, and audio-video products accounted for US$251.2 billion, while electronic parts accounted for US$222.9 billion. Together, the two categories represented 74 percent of all exports. The Ministry of Finance tied the surge to AI applications, cloud infrastructure, advanced chips, and high-performance computing.

The success is real. So is the uneven way it reaches people.

Government household-wealth data show that the top 20 percent of Taiwanese households held 62.68 percent of total household wealth in 2021, while the bottom 20 percent held 0.94 percent. Household net worth rose to NT$183.7 trillion in 2024, with the stock-market rally a major driver. This is how the boom moves: AI demand lifts chip exports, profits, and market valuations. Those gains then flow most strongly to households that already own stocks, property, or business equity.

The grandmother renting in Banqiao, the service worker in Kaohsiung, the cram-school teacher in Taichung, and the young couple deciding whether they can afford a child all live inside the same national success story. Most do not own much of its fastest-growing assets.

Taiwan’s technology firms have done nothing wrong by succeeding. The failure would be political: allowing a publicly enabled boom to compound through a narrow ownership structure while telling everyone else that GDP growth will eventually reach them.

In a recent BIEN article on Taiwan’s AI debate, I separated three policies that are often blurred together. Universal Basic AI distributes productive capability. Basic income distributes purchasing power. A public wealth dividend distributes ownership income. Taiwan needs all three discussions because they solve different problems. AI access helps a person use the new tools. Cash gives that person bargaining power and room to pay bills. Public shares answer the deeper question of who owns the return.

Taiwan keeps choosing cash, but not permanence

Taiwan has already normalized universal cash more than most countries. It paid NT$6,000 in 2023 and NT$10,000 in 2025. A third NT$10,000 proposal, estimated to cost NT$236 billion, cleared a first reading in May and remained in committee when I wrote about it in early July.

This is a real political change. Universal cash is no longer an idea that belongs only to basic-income advocates. The KMT and TPP have pushed it. The DPP government has resisted some versions and implemented others. Townships have paid their own local dividends and are discussing more. Whatever label politicians use, Taiwanese voters now understand what it means for a government to send the same cash payment broadly and without a poverty test.

But repetition is not permanence. Each payment still requires a fresh crisis, surplus, legislative fight, or election-season justification. As I wrote in the latest BIEN piece, “A handout is a windfall they hope arrives again.”

A sovereign wealth fund can change that relationship. It can turn an occasional payment into a claim supported by assets and governed by a formula. Cash would no longer depend entirely on whether politicians find another surplus and agree to share it.

Still, cash should not be subordinated to investment. UBI Taiwan’s work with a single mother made that obvious. The NT$10,000 monthly payment helped her buy a desk for her son, improve the family’s food, leave an unstable sales job, spend more time at home, and maintain one predictable source of support during cancer treatment. The pilot did not prove a national policy based on one family. It showed what conventional measures miss: flexibility changes the order in which a person can confront problems.

The same distinction now appears in Taiwan’s child-policy debate. A future investment account can build capital for adulthood. A monthly allowance can pay for food, rent, school expenses, transport, and care today. The stronger design combines them. A child cannot eat compound interest, but cash alone does little to close the inherited-asset gap.

The sovereign wealth fund should apply that lesson to the whole population: liquidity now, ownership over time.

Two ledgers, one public fund

Under my proposal, every eligible citizen would receive a locked allocation of non-transferable Public Wealth Shares. These core shares would represent a beneficial claim on a defined portion of the fund’s distributable returns. They would not give a person the right to liquidate the national portfolio.

The protections should be strict. Core shares could not be sold, transferred, pledged as collateral, seized by a private creditor, or redeemed early. They would remain attached to the citizen, not to a household, employer, bank, or political party. At retirement, the core shares could convert into a capped annual drawdown or lifetime-income stream. A lump-sum exit would defeat the point.

Then comes a separate personal ledger.

Each year, the core shares would generate dividends. A citizen who needs the money could take it as cash. A citizen who does nothing would have the distribution reinvested by default into additional personal shares or units linked to the fund. Those additional shares, and the gains they generate, would be personal and redeemable under clearly published rules.

The two ledgers solve different problems. Core shares keep the public inheritance intact. The personal ledger lets people compound wealth without trapping every dollar until old age. Someone facing rent, medical bills, or a job transition can take cash. Someone with more room can let the account grow.

This resembles a reverse Roth IRA only at the level of interface. A Roth generally allows access to contributed principal while restricting some earnings. Here, the publicly credited base shares are the protected part, while distributions and voluntarily accumulated additional shares are more liquid. The analogy is useful because people understand a protected retirement asset with tax-advantaged growth.

Why the default should be reinvestment, not compulsion

Public ownership changes how people relate to economic growth. Sam Altman made the case plainly in his proposal for an American equity fund: “the best way to improve capitalism is to enable everyone to benefit from it directly as an equity owner.” He also argued that assets rising with the country give people a literal stake in national success. OpenAI has reportedly held early-stage discussions about contributing a 5 percent stake to the U.S. government; no agreement has been announced.

Altman’s proposal is not a blueprint for Taiwan, and ownership does not automatically make every citizen patient, informed, or politically cooperative. But the underlying point is sound. A cash transfer helps a person spend. An asset gives that person a reason to pay attention to what produces the return.

Defaults matter too. Research on automatic 401(k) enrollment found that automatic enrollment sharply increased participation and that default contribution and investment choices strongly shaped what workers later did. The lesson is not that the state should remove choice. It is that a sensible default can help people follow through on a long-term interest while preserving a simple opt-out.

The same pattern appears among lower- and middle-income savers. In an H&R Block field experiment, IRA participation was 3 percent without a match, 8 percent with a 20 percent match, and 14 percent with a 50 percent match. Average contributions rose fourfold and sevenfold in the two match groups. The researchers emphasized simple, understandable incentives and accessible saving vehicles.

Taiwan’s proposal would differ from both studies, but the design lesson carries over. Credit everyone with an asset. Make reinvestment the default. Keep the cash election obvious and frictionless. Do not punish people who need the money today, and do not assume everyone will build assets if the system requires repeated paperwork and financial expertise. This model is complementary to Lai’s child allowance proposal, which provides cash and allocates a portion to locked savings until the child comes of age.

Cash and investment are sometimes presented as rivals because they appear in different ideological boxes. They are complements. Cash protects autonomy during the month a person is living through. Investment changes what that person owns five, ten, or thirty years from now.

Foreign reserves are not free money, but they are not a religious object

Taiwan held US$597.15 billion in foreign-exchange reserves at the end of June 2026. Any serious sovereign wealth fund debate has to confront that balance sheet.

The Central Bank is right about the basic distinction. Foreign reserves and a sovereign wealth fund have different jobs. Reserves provide external liquidity, support orderly currency markets, and help the country withstand capital outflows and financial shocks. A sovereign wealth fund accepts more risk to build long-term wealth. The Bank has also warned that its reserve assets correspond to liabilities, so they should not simply be handed to another institution without compensation or a proper legal structure.

That does not settle the policy forever.

Taiwan should not treat US$597 billion as a pile of idle cash. It also should not declare every dollar permanently unavailable for a national wealth strategy. The prudent position lies between those claims.

The government should publish a conservative reserve-adequacy band that accounts for import cover, short-term external debt, broad money, foreign portfolio exposure, plausible capital flight, exchange-rate pressure, and Taiwan’s unusual geopolitical and blockade risk. The assumptions should be public. The Central Bank, Ministry of Finance, NDC, independent economists, opposition parties, and national-security officials should be forced to debate the same stress scenarios rather than trading slogans.

Only reserves demonstrably above that band should enter the sovereign wealth fund discussion. Any transfer should be paid rather than confiscated, capped over time, authorized by statute, and reversible in a severe crisis. The fund could issue interest-bearing government claims to the Central Bank, or the government could purchase foreign assets from it through an explicit fiscal transaction. The exact plumbing matters because pretending away the Bank’s liabilities would hide the cost rather than eliminate it.

Citizen prosperity should be the first objective of economic policy. Financial stability is part of that prosperity, not an obstacle to it. A reserve policy that leaves Taiwan unable to handle an external shock would betray citizens. A reserve policy that accumulates far beyond any defensible safety requirement while households remain excluded from national wealth would also deserve scrutiny.

The right question is not “Can we raid the reserves?” It is “How much insurance does Taiwan need, under what scenarios, and what should it do with a verified excess?”

Taiwan is already using public finance to help firms globalize

The government is not waiting for the sovereign wealth fund to use public balance-sheet capacity. The National Development Fund has already doubled its overseas investment financing loan envelope from NT$30 billion to NT$60 billion, supporting Taiwanese firms as they expand abroad. The government is also building AI infrastructure, supporting strategic industries, and coordinating land, energy, water, credit, and diplomacy around technology investment.

Those policies may be justified. They also expose the missing half of the bargain.

A financing guarantee helps a company borrow. A subsidy lowers a company’s cost. A science park creates infrastructure around a company. None of those instruments gives citizens a direct asset.

Future strategic support should therefore carry public upside when the scale is exceptional. Large subsidies, preferential land, infrastructure commitments, emergency guarantees, or bespoke utility investments can include warrants, equity, royalties, or revenue participation negotiated in advance. If the public absorbs unusual risk, the public should retain something that appreciates when the bet succeeds.

This is not a retroactive seizure of TSMC or an excuse to micromanage firms. It is the contractual logic Taiwan used at the birth of its semiconductor industry, updated for a mature, capital-intensive economy.

What Alaska and Norway teach Taiwan

Alaska remains the closest political example because its Permanent Fund makes public wealth visible. Residents receive an annual cash dividend, and the 2025 payment was US$1,000. The payment is not large enough to replace work or the welfare state. It is large enough to tell every resident that oil wealth belongs partly to them.

The evidence also answers one predictable objection. Damon Jones and Ioana Marinescu found that the Alaska dividend did not reduce aggregate employment. Part-time work increased by 1.8 percentage points, consistent with the payment supporting local demand and giving some people more flexibility.

Alaska’s weakness is political. The dividend has become entangled in annual budget fights, and the amount changes sharply. Taiwan should copy the visibility and avoid the instability. The distribution formula belongs in law, tied to smoothed long-term returns rather than the mood of the legislature.

Norway offers the opposite half of the model. Its Government Pension Fund Global invests abroad, diversifies widely, and uses professional management. Its fiscal rule aims over time to limit government spending to the fund’s expected real return, currently estimated at 3 percent. It does not pay an individual Alaska-style dividend. Taiwan should borrow Norway’s discipline without copying its distance from citizens.

My preferred synthesis is simple: Norway’s governance, Alaska’s citizen visibility, and Taiwan’s own developmental-state tradition of taking public ownership when the state helps create an industry.

Bernie Sanders has pushed the ownership question into American politics with a proposed AI sovereign wealth fund financed by a one-time 50 percent stock tax on major AI companies. He is right that AI wealth rests on collective knowledge and public investment. Taiwan should not copy the mechanism. A forced 50 percent equity transfer with public voting power exercised through an independent commission would be destabilizing for strategic, capital-hungry semiconductor firms.

Taiwan’s version should be quieter and more durable: negotiated public stakes in future support, a portion of boom-year revenue, a carefully debated reserve contribution, diversified investment, and locked citizen shares that cannot be sold to the highest bidder.

A practical funding and governance rule

A Taiwan Public Wealth Fund should have several funding channels rather than one politically convenient target.

First, a fixed share of exceptional boom-year revenue should flow automatically into the fund. When corporate income tax, securities-transaction tax, or total revenue exceeds a rolling multi-year trend by a defined margin, the statute should reserve part of the excess for permanent investment. Taiwan still has defense, infrastructure, debt, healthcare, and social needs, so the share should be meaningful without swallowing the entire surplus.

Second, major future public support should carry upside instruments where appropriate. That can mean equity, warrants, royalties, or revenue sharing. The terms should be known before a firm accepts the support.

Third, a limited foreign-reserve contribution can be considered only after the adequacy test described above. The amount should be transparent and phased, not chosen to fill a political funding target.

Fourth, new capital should be invested globally. Taiwan’s economy, tax base, labor market, stock market, and existing public assets are already concentrated in semiconductors. A public fund that simply buys more of the same exposure would magnify the national risk. Global equities, fixed income, infrastructure, and other assets can convert a concentrated domestic windfall into a more stable public inheritance.

Governance has to be harder to capture than an ordinary ministry program. Taiwan should follow the Santiago Principles and add an independent board, staggered appointments, professional managers, published benchmarks, audited accounts, conflict-of-interest rules, legislative oversight, and a ban on directed election-year lending. No president or legislative majority should be able to turn the fund into a four-year patronage pool.

The distribution rule should use smoothed real returns over several years. That allows a predictable dividend without forcing asset sales after a market crash. A fixed portion would support citizen distributions and personal reinvestment accounts; the rest would compound inside the collective fund.

The politics are more open than they look

That creates room for a cross-party ownership bargain.

The DPP can turn Lai’s sovereign wealth fund announcement and shared-prosperity language into a benefit people can actually see. The KMT can argue that permanent ownership is more fiscally conservative than recurring ad-hoc handouts. The TPP can insist on formula-based governance and a citizen account that is easy to audit. None of the parties has to surrender its identity to support the same institution for different reasons.

The alternative is less attractive. The government can build financing platforms for companies, accumulate assets at the state level, and promise that the gains will eventually improve society. The legislature can keep fighting over one-off cash whenever a surplus appears. Citizens remain spectators in one system and supplicants in the other.

A public share changes the relationship. Taiwan’s AI economy stops being only a sector people work around, a stock they may not own, or a national achievement they are expected to applaud. It becomes an asset in which they have a protected claim.

The bottom line

Lai has proposed the vehicle. Taiwan now has to decide who rides in it.

The strongest design gives every citizen locked Public Wealth Shares, protects those shares from sale and private capture, and generates an annual distribution that can be taken in cash or reinvested by default. The reinvested personal shares remain accessible under clear rules. The core public inheritance stays intact and can support retirement income later in life.

That combination matters. A public fund without a dividend leaves citizens as spectators. Cash without an asset base remains vulnerable to the annual budget fight. Taiwan can build both forms of security in the same institution.

The reserve question should be debated honestly. Taiwan needs ample protection against financial and geopolitical shocks. It should also be willing to ask whether reserves above a published, conservative adequacy band can be converted into diversified public wealth. Stability and prosperity are not opposing goals. Both exist to serve the people.

Taiwan’s government helped finance the company that now anchors the global AI economy, and the public still owns a valuable piece of it. The country has already proved that strategic public investment can build world-leading productive capacity. The next task is to apply the same seriousness to ownership.

Taiwan helped build the mountain. The people should receive a share of what it produces.